Apple at 50: How one company turned near-bankruptcy into a $3.5 trillion institution — and what it teaches every long-term investor

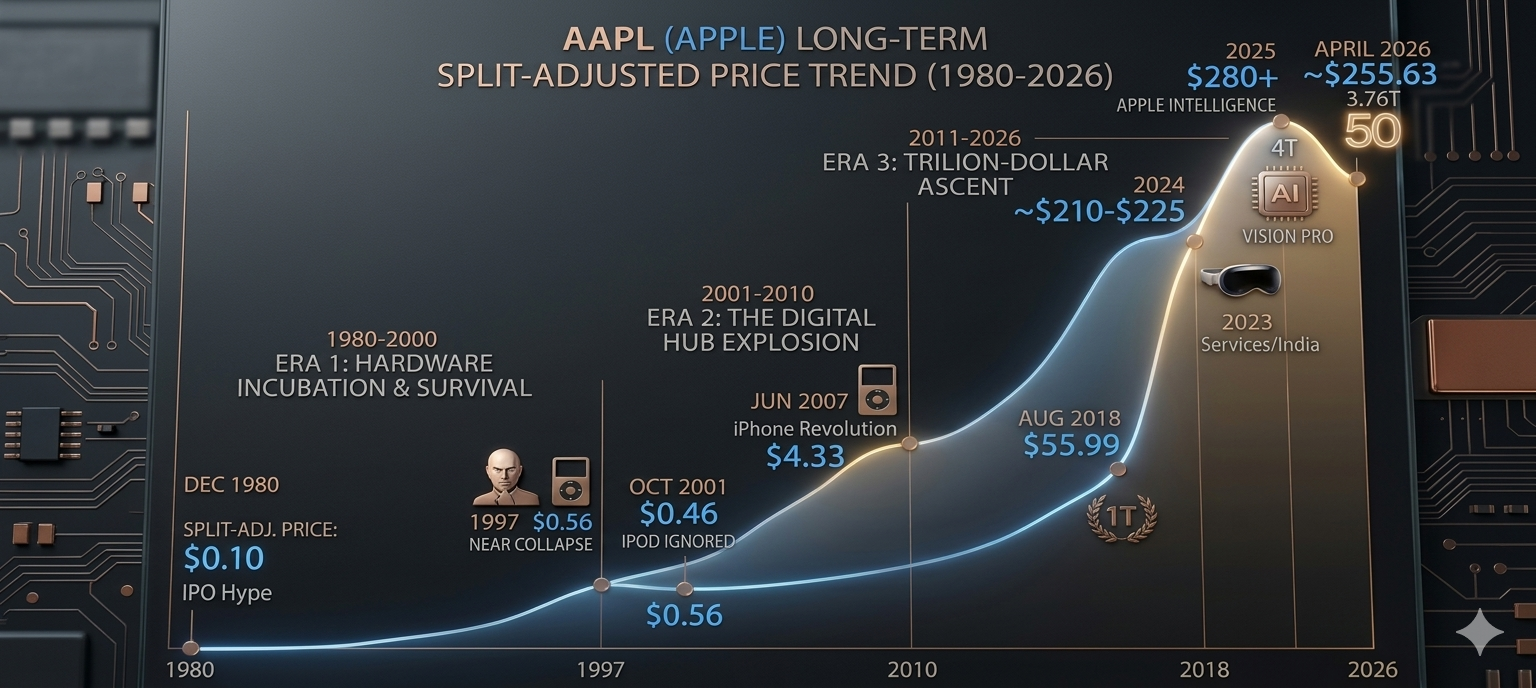

Look closely at the visual above.

The repeated, deliberate reinvention of what Apple is and how it earns.

Over 50 years, Apple didn't just launch products. It kept changing its engine of growth:

Computers → Portable Devices → Ecosystem → Services → In-House Silicon

Each shift strengthened the same three pillars: control, margins, and customer stickiness. That is why the financial curve does not just grow — it accelerates.

Here is a number worth sitting with:

Apple's split-adjusted IPO price in 1980 was $0.10 per share. In January 2022, it hit $182. That is an 1,820× return in 44 years.

But the path was never straight. And that is precisely the point.

The per-share journey :

All prices are split-adjusted across Apple's five stock splits (1987 · 2000 · 2005 · 2014 · 2020). The nominal IPO price was $22.

The Dip Before the Boom: A Lesson for Today's Market

We are in a period of market anxiety right now. Valuations are under pressure. Investors are asking: how much lower can this go?

Apple's own history offers a counter-intuitive answer.

In October 2001, when the iPod launched, Apple's share price was $0.46 — lower than it had been four years earlier when Jobs returned to save the company. The stock did not react. The transformation was invisible to the market.

Within six years, the same share was worth $4.33. Within twenty, it was worth $182.

This is the pattern that repeats across great compounders: the stock goes quiet, or even dips, precisely at the moment the business is doing its most important work — repositioning, reinventing, laying the foundation for the next era of growth.

The investors who waited for certainty before buying missed the entire move. The ones who bought when the story was unclear captured the compounding.

The question is never when will the market hit bottom. The question is: is this business becoming something better?

What Warren Buffett Saw That Most Missed

Berkshire Hathaway began building its Apple position in early 2016, when the stock was trading at roughly $25 per share — battered by fears of iPhone saturation and slowing growth.

Buffett's rationale was not about a product supercycle. It was about something more durable:

He saw a consumer ecosystem with switching costs so high that customers would not leave even if the hardware stopped improving. He was not buying a phone company. He was buying a habit.

By 2018, Berkshire had invested approximately $36 billion in Apple. By 2023, that stake was worth over $177 billion — the single largest position in the Berkshire portfolio, accounting for nearly 50% of its equity holdings at peak.

Buffett has since called Apple his best business investment. Not because he predicted the iPhone 15 or Apple Intelligence. But because he identified the compounding engine underneath the product headlines.

The lesson: the best entry points rarely feel comfortable. In 2016, Apple looked tired. That was the window.

Why the Curve Accelerates

Apple's revenue grew from $8 billion in 2004 to $391 billion in 2024. But the composition changed completely:

2007: Mac = 43% of revenue. iPhone = 2%.

2024: iPhone = 51%. Services = 25%. Mac = 8%.

Services grew from near zero to $96 billion annually — higher margin than any hardware.

Each era of Apple did not simply add revenue. It added a higher-quality layer of revenue — more recurring, more profitable, more defensible. That is why the financial curve does not grow arithmetically. It compounds.

The Real Question

Most people try to time the market or chase the next big product. Long-term wealth is created by identifying businesses that are continuously evolving — and staying invested through the transitions.

Apple's 50-year journey is not a story about technology. It is a story about a company that refused to be defined by its last product — and kept building the next version of itself before the world knew it was needed.

Even the promoters — the founders, the early employees, the first investors — did not know how far it would go. Nobody who bought at $0.10 expected $182. What they saw was a company that was different. That was enough.

At FINSTREET, this is exactly what we focus on — not just what a company is today, but what it is becoming next.

Are you investing in what a company is today — or what it is becoming next?

#Apple50 #Investing #LongTermThinking #Finstreet #StockMarket #WealthCreation #WarrenBuffett #MarketAnalysis